Money

Friday, January 12, 2024 • 9 min read

I’ve used some version of Quicken for 35 years. That puts me in a stodgy demographic that manages money in a certain “this is how I’ve always done it” way. For the uninitiated, Quicken is a personal finance software program that helps manage your checkbook and credit cards, pay your bills, keep to a budget, and track investments. It’s available on Windows and Mac, though there are differences in capabilities between the two. There are companion apps for iPhone and iPad, but they feel like afterthoughts, lacking key functionality of the desktop software. Quicken Classic is sold as an annual subscription across three offerings: Deluxe, Premier, and the recently released Business and Personal edition.

Seven years ago, I switched from Quicken Premier for Windows to the less capable Mac version. I’ve written previous blog posts about using Quicken on the Mac: in early 2018 when I switched and follow-on updates in 2019 and 2020. In large part, I was critical of the Mac version of the software, particularly its inability to export investment data.

In the intervening four years since my last post, Quicken has improved in many ways, including the ability to export all its data, including investments, to Quicken for Windows. With this critical functionality in place, I thought it was time to provide an updated and favorable review of the Mac version of Quicken and how I rely on it to manage almost every aspect of my financial life.

Why Quicken

I began my career in public accounting and held a CPA license in Washington state for over thirty years. I spent most of my career as a finance executive with a large publicly traded company, which allowed me direct experience with stock options, restricted stock units, performance shares, deferred compensation plans, and various employee benefit programs that follow that kind of employment. I’ve always tried to be disciplined when it comes to money, and I’m comfortable managing my own finances. With this background and financial situation, I have had many opportunities to evaluate and push the boundaries of Quicken as a personal finance program.

It takes time and expense to maintain a system like Quicken. Many manage their money with simpler apps or just by scanning their accounts online. For me, the effort of a system is worth it. With Quicken, I know what’s going on with my spending and income in relation to expectations every week. Every expense has a monthly budget that fits within a long-range plan. The impact of gyrations in the stock market is personalized with a press of a button. My entire financial history is accessible from Quicken’s search bar. Bills always get paid on time. Checks never bounce. I am rarely surprised at the end of a month, quarter, or year. The peace of mind I get from using Quicken far outweighs the cost.

As a disclaimer, I don’t work for Quicken or have any financial interest in the software or related services. Quicken doesn’t offer a free trial to evaluate, so unbiased reviews from actual users are helpful. I read almost everything I could find before switching to the Mac in 2018. Consider this update an act of paying it forward.

Recent Improvements

Since 2020, there have been dozens of software updates to Quicken. Unlike those early years when I first moved to the Mac, Quicken has now become a pleasure to use, and I consider it a stable, trusted system. Here are a few of the improvements that made the most significant impact on my use:

Error-free Transaction Downloading. The team at Quicken has vastly improved the technology involved in downloading transactions from banks, credit card companies, and brokerage firms. When I first used the Mac version, download errors would pop up continuously. Those days are happily behind me. I'll go weeks and months between download errors, which seem to resolve after a day. My experience is limited to just a few institutions, so your own mileage may vary.

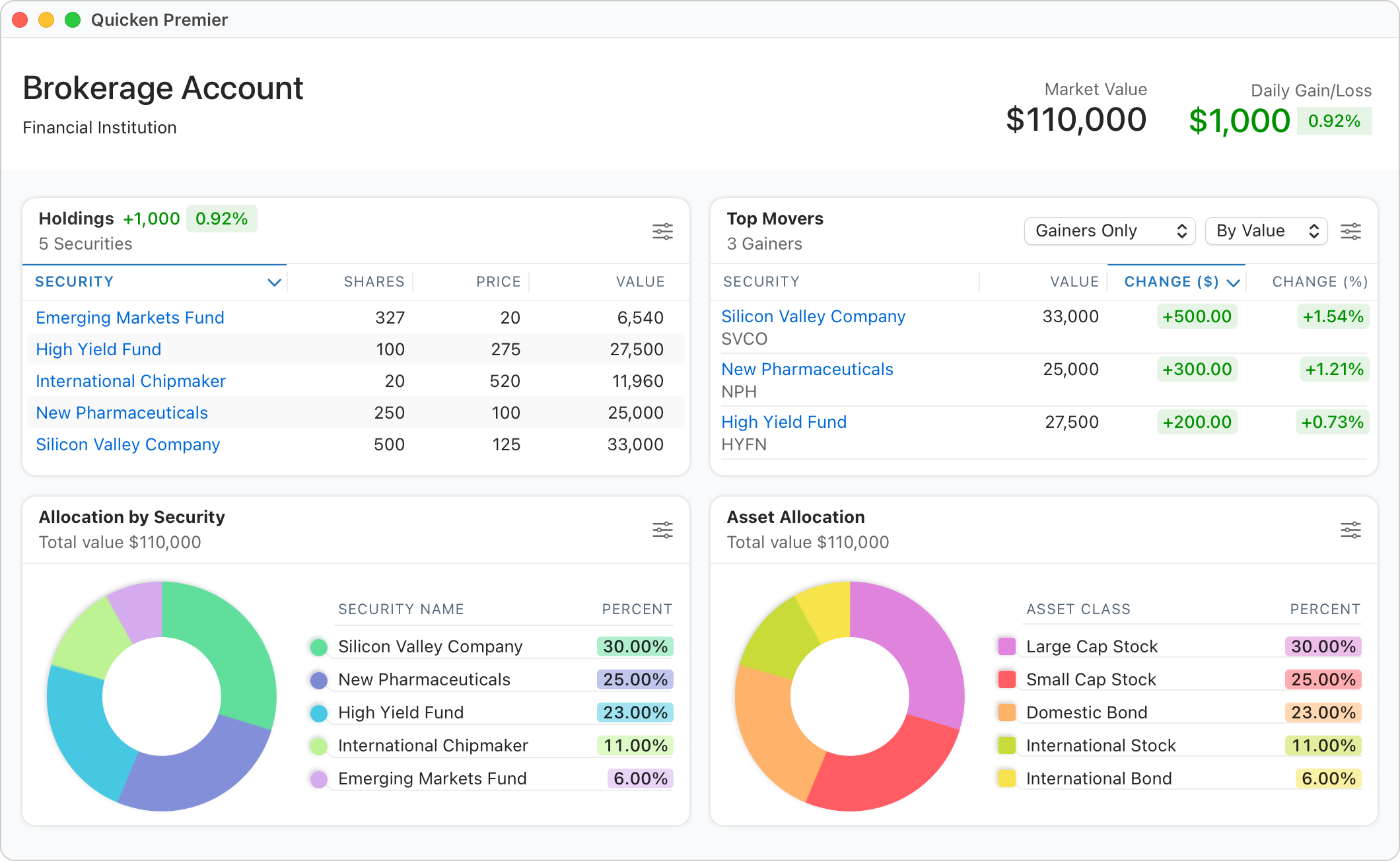

Investment Analysis and Dashboards. The Mac software now provides overall investment allocation between stocks, bonds, and cash, even with mutual funds that own a blend of assets. This update essentially removed the need for me to separately analyze my investments in Excel. In addition, a new dashboard provides a valuable snapshot of investment performance and holdings that rivals and, in some ways, exceeds my brokerage tools. Quicken’s investment section has become quite good.

Bill Manager. Quicken has refined its bill tracking and payment capabilities in a big way. The Premier version of Quicken offers free bill paying, but I prefer to send these occasional checks directly from my bank. I use their bill manager service, though, which does some pretty innovative things. First, it can download PDF statements automatically without having to log in to the payee’s website each month and hunt around for the statement. It also automatically schedules the payment based on the due date and records in the payment register. You can make payments directly from Quicken, but my recurring bills are paid automatically, so recording the transaction is all I need. A couple of companies I pay aren’t included in Quicken’s Bill Manager service, but these can be added manually. Second, I get a nice cash balance forecast as these future bill payments are scheduled in the register, preventing possible overdrafts or shortfalls. Bill Manager solves a problem I didn’t know I had, and I’m glad I have it.

Snappy Performance. The software runs faster thanks to performance improvements, particularly with newer Silicon Macs. I use Quicken on an M1 MacBook Air and an M2 Mac Mini. Both perform exceptionally well.

Investment Data Export. Until late last year, Quicken for Mac’s export capabilities excluded investment data. This meant I could not move back to Quicken for Windows or any other competing personal finance apps without losing all my investment history. I hated having to rely on this one particular version of software for all my precious financial data. Luckily, Quicken has now fixed this shortcoming, and Mac users of the software can breathe a collective sigh of relief.

Mac Version Still Lags Windows

Despite the many improvements to the Mac version of Quicken, it still lags behind the Windows version in a few key areas:

- Reporting in the Windows version is more robust, customizable, and allows comparisons to budget.

- Windows Investment analysis is more in-depth with Morningstar Portfolio X-Ray and performance benchmarking.

- Tax Center in Windows makes income tax planning easier by calculating estimated taxes using actual tax brackets on recorded income.

Other planning tools like Lifetime Planner, Debt Reduction, and Savings Goals haven’t made it to the Mac yet, but these tools always felt a little gimmicky. I didn’t use them on Windows, so I don’t miss them on Mac.

Quicken Risks and Alternatives

This is an interesting time for legacy software companies like Quicken. I suspect their loyal customers look a lot like me: retired or near retirement, comfortable with desktop apps, lugging along a decade or more of historical data within their app, and resistant to change.

Most new entrants into the personal finance technology space are mobile app-centric. Some don’t even offer desktop apps. Quicken has recently entered this space with its Simplify mobile app and likely believes it represents most of its future growth, which explains why it recently rebranded its desktop software to Quicken Classic.

Intuit, the former parent company of Quicken, recently announced the shutdown of its personal finance app, Mint. Mint is one of the most popular and longest-running app-based finance tools, so its demise sent shockwaves through its customer base. Indeed, this announcement caused me to look more carefully at my use of Quicken and think through what steps I would need to take if the service were similarly shuttered.

I think that the risk is relatively low. Aquiline Capital Partners acquired Quicken in 2021. Typically, private equity firms maintain ownership from five to seven years, so Quicken is in the sweet spot of ownership. Aquiline will be focused on investment and growth vs. the cost-cutting and profit harvesting that comes near the end of the investment horizon as they look to sell their asset. This is good news for Quicken’s current customers.

And yet, I can’t help but feel that users of Quicken software are on borrowed time. Highly regarded mobile apps like Monarch Money and Copilot will continue to improve and introduce more and more capabilities. Eventually, Quicken will be forced to mothball its desktop software as everything moves to the cloud and apps. This is one of the reasons I’m happy that Quicken for Mac’s export function now includes investment data. I might not need this now, but someday I will.

As a safeguard, I create and archive two export files from Quicken every quarter. One is simply the Quicken Transfer File (QFX) you can export from the file menu. I also download a CSV file of all my Quicken transactions by selecting All Transactions from the sidebar and choosing Export Register Transactions to CSV from the File menu. This yields a 60,000-row text file I can access with Excel to search and sort every transaction stored in Quicken for the past 30 years. Between these files, I’m confident I could move my history to a new finance app without too much trouble, even if Quicken stopped working altogether.

Recommendations

Quicken Classic for Mac has a lot going for it in 2024. The software is intuitive, stable, and a pleasure to use. I am pleased with Quicken’s decision to allow a complete export of my data, including investments, should I ever need it. As a Mac user, I have no desire to revert to the more capable Windows version through Parallels or some other clunky virtualization process.

Quicken’s subscription cost is fair for the value I receive, and the frequent updates are delivered almost monthly (as I write this, Quicken released Version 7.5.0, which introduced more new enhancements). Almost all personal finance apps use a subscription business model, and many are more expensive than Quicken. Buying an annual license during Black Friday sales in November can save 30-40% off the regular subscription rate.

For someone with 30 years of history with Quicken, I’m in no mood to switch platforms, given the state of the app today.

And yet, if I were just starting out, would I choose Quicken? I doubt it. From a clean slate, I would probably choose one of the more innovative mobile apps that deliver the power of personal financial management to your pocket or tablet. I plan to test drive a few of these over the coming year to better understand these next-generation tools.

Until then, Quicken for Mac will remain my everyday companion and financial advisor. If you’re a long-time Quicken for Windows user considering switching to the Mac, it’s an excellent time to make the leap.

Monday, November 9, 2020 • 11 min read

Welcome to my third annual review of the personal finance software, Quicken for Mac. I have been using Quicken to manage my finances since 1989: first on the Mac, then a long stint on the Windows version, before switching back to the new-and-improved Mac version four years ago. I wrote about the process of switching from Windows to Mac here.

As I wrote then, I had very high expectations for the Mac version under new leadership, independent of Intuit, and the financial benefit of a new subscription-based business model. In this post, I’ll share an update on how it’s gone using the latest version, Quicken 2020 for Mac.

Unlike other written reviews of Quicken software, my recent experience is exclusive to the Mac platform, though I will make feature comparisons to the Windows version. If you’re a Quicken Windows version thinking about switching over to the Mac, this review should be useful.

My Background

I began my career in public accounting, and while I no longer provide accounting or auditing services to clients, I’ve held a CPA license here in the state of Washington for over thirty years. My finances mirror those of many mid-life families eyeing retirement: a half-dozen investment and retirement accounts, college savings accounts, a home, etc. My work for a publicly-traded company for the past twenty years has allowed me direct experience with stock options, restricted stock units, performance shares, deferred compensation plans, and a variety of employee benefit programs that follow that kind of employment. I’ve always tried to be disciplined when it comes to money, a natural-born planner, and I’m comfortable managing my own finances. With this background and financial situation, I have had many opportunities to evaluate and tug at the boundaries of Quicken as a personal finance program, particularly on this evolving Mac version of the software.

Quicken for Mac - An Evolution

For most of my time on Quicken, I used the Windows flagship version of the program. I switched over to Mac for most things almost twenty years ago, except Quicken. Back then, Quicken on the Mac was too basic for my needs. Instead, I used a virtualized version of Windows inside the Mac to use Quicken. Each year I would await the latest incarnation for the Mac, only to be disappointed by the one-star feedback of early adopters on the Mac App Store. I finally took the leap in 2016 after Quicken 2017 for the Mac was released, and initial feedback was mildly positive for the first time. I planned to run parallel systems between Mac and Windows, but that became too much effort, so in January 2017, I switched entirely to Quicken Premiere for the Mac. I chose the high-end version because I needed the investment accounting and tracking features.

Let me be clear about something before I get into what’s changed in the latest version of Quicken. With all its shortcomings, Quicken is still superior to any other personal finance program on the Mac if you need robust investment tracking. There may be better cash flow and budgeting software (Banktivity and YNAB, for example), but these apps fall short, in my view, of keeping tabs on the intricate accounting treatment for the variety of obscure transactions that flow from owning stocks, mutual funds, stock options, and employer-granted restricted stock. For this type of financial management, Quicken is still the only consumer-targeted personal finance software game in town.

Quicken 2020 for Mac and the Subscription Business Model

Since my last review of Quicken for Mac 2019, there have been seven updates to the software, occurring every four months or so. These updates, both major and minor, have continued to push the Mac platform forward, perhaps even narrowing the gap between its Windows big brother. I am heartily glad of this development. When Quicken launched its subscription business model in 2016, many customers (myself included) were concerned that that the software would languish, and all the subscription revenue would simply pay down leveraged debt, now that the Quicken corporation was owned by private equity .

I subscribe to the Premiere version of Quicken, which lists for $80 per year on Quicken’s web site, though I’ve never spent anything close to that in renewals. I typically renew in November and watch for Black Friday sales at Amazon. This has brought my annual cost to around $40, which I consider a bargain given how much I rely on this software.

I remain vigilant, however. Quicken’s private equity ownership period hits the five-year mark in April 2021. Private equity firms typically sell their investments after a five to seven year holding period, and a company being offered up for sale is often tempted to dress up its profits by deferring expenses or cutting staff. We’ll have to wait and see if this happens with Quicken.

New Features in Quicken 2020

Web Access. Touted as their number one feature request, Quicken introduced access to your financial system via the web in 2019. This is surprisingly robust and complete. Online transactions from bank and credit card accounts can be downloaded, just like on your Mac, and any edits you make to transactions sync to the desktop version. It doesn’t appear you can pay bills from the web platform, nor can transactions from investment accounts be downloaded. But it’s a handy tool to check in on your finances while traveling without having to pack a computer (access on an iPad Pro using Safari was fine). One glaring omission is two-factor authentication as a security measure. Having access to all your financial data with just a simple user name and password feels very risky. I’ve turned off web access for this reason, but will turn it back on when better security measures are in place.

Bill/Check Pay. Quicken revamped its bill-pay functionality in 2020. Paying bills from within Quicken is only available for Premiere subscribers, and the previous incarnation made no sense to me. I’ve tinkered with the new version, but haven’t used it. My current process for online bill paying through my bank works well enough for me.

PDF Bill Downloading. Another new feature is Quicken’s ability to automatically download bills and credit card statements in PDF format for review and filing. This is a convenient way to access these bills without having to navigate to the vendor’s web site, type in credentials, and search for the latest bill or statement. It seems to work well, unless it doesn’t. For some reason, it won’t download my cellphone statement from AT&T, though it knows how much it is. Of the dozen vendors I set up, it provided a PDF about half the time. This feels like a work-in-progress, but it should improve over time.

Improvements and Updates

Reporting. Quicken made some improvements in reporting available on the Mac in their newly designed Report Center. Reports are now better organized and easier to customize and save. A few additional reports were created, but sadly, we still don’t have any budget to actual reports, which is a mainstay of personal financial management.

Transaction Renaming Rules. Long a sore spot on the Mac, Quicken added some new functionality in properly renaming downloaded transactions. This is a welcome addition. For years, I would shake my head as Quicken would stubbornly refuse to learn the proper expense category for the utility bill I download and pay every month. That has mostly been corrected now with their new transaction renaming engine (a bug still persists that makes Quicken unable to remember transfers to other accounts as part of a memorized transaction). They’ve even added some power-user techniques to suss out the proper renaming of some of the more bizarre credit card transactions I routinely see, particularly with Apple Pay transactions I pay with my watch. Here’s an example transaction from a grocery store purchase:

AplPay VASHON THRIFTVASHON3402234

The new renaming rule I created scans for two bits of text: “AplPay” and “THRIFTVASHON”. If those two rules match, it renames the transaction to “Vashon Thriftway”. The renaming engine can even look back into history and apply these rules to clean up old transactions. This was a very helpful addition.

Budgeting Improvements. Quicken’s budget tool received an important update. You can now include account transfers and investment income in your annual budget. This is especially important for retirees or those soon approaching retirement age.

What’s Still Lacking or Needs Improvement

Reporting, Particularly Against Budget. Reporting in the Mac version of Quicken has improved, but you can’t create a report of your actual results vs. budget, which is an essential financial planning tool. Instead of a report, you get a bizarre on-screen (and unprintable) visualization of budget performance for the month, or an unwieldy 12 month stacked grid, neither of which I find at all useful. Unless you happen to view the 12-month screen on the very last day of the month, the year-to-date totals are useless: the budget total includes the full budget for the month you’re viewing vs. month-to-date actual results. I’ve been waiting for this basic actual vs. budget report since 2016, a report that has been available in the Windows platform forever. How in the world can a software program designed to help individuals and families manage their personal finances not include a budget to actual report?

Tired of waiting, I now export actual and budget figures out of Quicken to create a proper actual vs. budget report in Excel. I took the time to automate the workbook in 2019, so it takes just moments to create. Of course, my Excel hack lacks interactivity and drill-down capability, which is important in tracking down the source of budget variances.

Quirky Transaction Download Errors. Every time I do an online update of my accounts, I receive the same throttling error for a random set of accounts with my primary bank. I have a half-dozen banking, savings, and credit card accounts with this bank, which is apparently too many for Quicken. I click the “try again,” and the process completes. I’ve researched this error online and discovered that many users suffer from this across a variety of financial institutions. Quicken’s response is consistent: “your bank’s servers must be busy. Try again later.” Downloading transactions in Quicken on Windows was always a tricky proposition, so I can’t say this is a Mac issue. Just irritating.

Morningstar Portfolio X-Ray. The Windows version of Quicken allows you to analyze your investment portfolio in much greater detail than on the Mac using Morningstar X-Ray. This tool looks inside your mutual fund investments to properly report your asset allocation (i.e. stocks, bonds, cash) and any concentrated positions of a security. This investment scrutiny is not available on the Mac. For example, if you own a mutual fund that invests in both stocks and bonds, you really have no way of knowing your actual asset allocation within Quicken. I’ve hacked together a way to export my investment holdings into Excel to accomplish this, but it’s another pain-point for investors using the Mac version of Quicken.

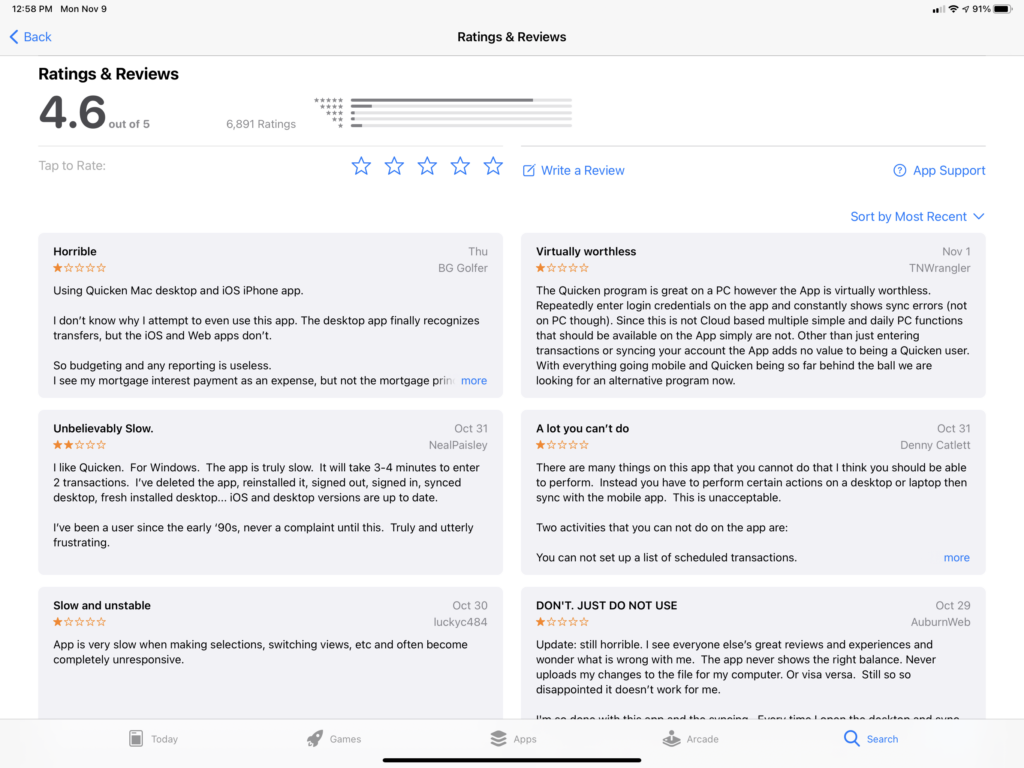

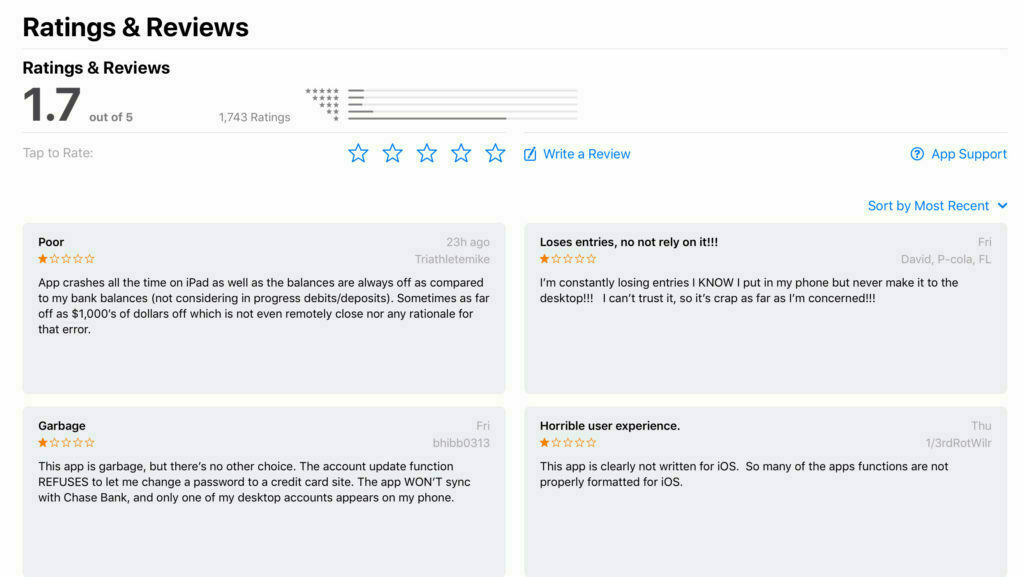

Mobile App is Underwhelming. Quicken’s iPad app has been out for a while. I tried it out when it first came out and was underwhelmed. I tried it again for this review, and I am still unimpressed. I’m not alone: the app ratings are abysmal with many reports of the app crashing or not being able to log in. The web view is much, much better.

Quicken for iPad suffers from poor user reviews …

Quicken for iPad suffers from poor user reviews …

Trapped Investment Data. One of the biggest reservations I have with the Mac version of Quicken relates to its file export limitations. While Quicken promises a “Data Access Guarantee,” the export functionality of the Mac program remains severely crippled. Investment accounts, and all the related historical transaction details, cannot be exported. This limitation affects not only your ability to move back to the more robust Windows version of Quicken should you grow tired of the Mac’s shortcomings, but also impacts your ability to switch to other personal finance software products on the Mac if you decide to give up on Quicken altogether. The lack of this basic export function feels intentional to me to keep customers from leaving the product.

If you are using the Windows version of Quicken and you have investment accounts, you should be very cautious before migrating to the Mac version. You’ll likely be able to move everything over to the Mac, but you’ll be stuck with limited choices of ever leaving. Shame on Quicken for taking our financial data hostage.

Closing Thoughts

After three years of using Quicken for Mac, where do I stand?

While there’s still plenty of room for improvement — say, a budget to actual report — Quicken is still the best consumer-level software for Mac users with complicated finances. Quicken for Mac is good enough that I’m not willing to go through all the work to revert back to the Windows version and deal with running a virtual PC on my Mac. I’m disappointed that my Mac data file can’t export to other software programs (or Quicken for Windows). I hope future Quicken versions will finally improve enough to be on par with Windows, though experience makes me very skeptical.

If you’re a Mac user with an investment portfolio, but still on the Windows version, I would recommend staying with that more robust software until the Mac version allows proper data exporting.

Are you a Quicken for Mac user, or a Windows user thinking of making the switch to Mac? Let me know your questions and feedback in the comment section below.

- Quicken was acquired from Intuit by HIG Capital in April, 2016. ↩

Sunday, January 6, 2019 • 10 min read

See my Quicken 2020 for Mac Review for the most recent review.

I have been using Quicken to manage my finances since 1989, making this my 30th anniversary with the program. Though I started on a Mac, and use a Mac today, the vast majority of my use has been on Windows. A little over two years ago, I switched to the Mac version of Quicken which I wrote about here.

As I wrote then, I had very high expectations for the Mac version under new leadership, independent of Intuit, and the financial benefit of a new subscription-based business model. In this post, I’ll share an update on how it’s gone using the latest version of Quicken, Quicken 2019 for Mac.

My Background

I began my career in public accounting, and while I no longer provide accounting or auditing services to clients, I am still a licensed Certified Public Accountant here in the state of Washington. My finances mirror those of many mid-life families: a half-dozen investment and retirement accounts, college savings accounts, a home, etc., though working for a publicly-traded company these past twenty years has also allowed me direct experience with stock options, restricted stock units, and a variety of employee benefit programs that follow that kind of employment. I’ve always tried to be disciplined when it comes to money, a natural-born planner, and I’m comfortable managing my own finances. With this background and financial situation, I have had many opportunities to evaluate and tug on the boundaries of Quicken as a personal finance program, particularly on this evolving Mac version of the software.

Quicken for Mac - A Painfully Slow Evolution

For most of my time on Quicken, I used the Windows flagship version of the program. I switched over to Mac for most things about 15 years ago, except for Quicken which initially wasn’t available at all, and early versions were either too basic or too buggy. I had to run Windows virtually inside a Mac which was a hassle, so I was eager to move to the native version of Quicken. Each year I would await the latest incarnation for the Mac, only to be disappointed by the one-star feedback of early adopters on the Mac App Store. I finally took the leap in 2016 after Quicken 2017 for the Mac was released, and initial feedback was mildly positive for the first time. I planned to run parallel systems between Mac and Windows, but that became too much effort, so in January 2017, I switched entirely to Quicken Premiere for the Mac. I chose the high-end version because I needed the investment accounting and tracking features.

Let me be clear about something before I get into what’s changed in the latest version of Quicken. While I take issue with how slowly the Mac version has developed, particularly in light of the abilities of its Windows counterpart, Quicken is still superior to any other personal finance program on the Mac if you need robust investment tracking. There may be better cash flow and budgeting software (Banktivity and YNAB, for example), but these apps fall short, in my view, of keeping tabs on the intricate accounting treatment for the variety of obscure transactions that flow from owning stocks, mutual funds, stock options, and employer-granted restricted stock. For this type of financial management, Quicken is still the only personal finance software game in town.

Quicken 2019 for Mac

Quicken 2019 for Mac was released with little fanfare in November 2018. Since I purchased a 20-month subscription to Quicken Premiere last year during an Amazon.com Black Friday sale, updates like the 2019 edition have been provided at no additional charge. I didn’t even notice the name had changed since it came through as a regular software update.

The software saw a half-dozen meaningful updates throughout 2018, suggesting the annual renaming to a new year is more marketing than substance these days. So, the improvements I’ll note here relate to software updates during all of 2018 vs. just since the 2019 rebranding.

What’s Better

Performance. Last year, I complained of performance delays when switching investment views and exiting this program. These lags have mostly been corrected. Quicken claims that portions of the program are four times faster in 2019. Opening and closing the program is much quicker, and, while I still see the occasional beachball icon when viewing investments, the overall program seems faster and more responsive. I’m using a newer iMac to run Quicken, so your mileage may vary, but my experience has been positive.

Investment Tracking and Analysis. Long a sore spot on the Mac, investment tracking and analysis continued to see updates in 2018. It’s been a while now since I’ve used the Windows version of Quicken, but I no longer feel like I lack analysis features for my investments. I can view investment returns by class of investment (stocks, bonds, cash, other), security, holding period, etc., and drill into lots of purchases for my original cost basis, current gain or loss, and most recent market changes. I’ve read reports that others are still having difficulty with accurate investment return results, but in my case, it’s working flawlessly. This is a big deal to me, and it’s nice to see the improvements Quicken made to the Mac platform.

New Export Capabilities. I have complained about the lack of decent reporting in Quicken for Mac and will discuss that more in the next section, but some of this has been mitigated by Quicken’s new export to Excel functions which are available in more areas now, including investments. This allows you to copy data out of Quicken into a spreadsheet for analysis and reporting. I’ve used this function for the past two years in creating my own “Budget to Actual” report in Excel, but now you can do this with a lot more of your financial data. I was never all that happy with even the most robust reporting available in Quicken’s legacy Windows product and found myself using this copy/paste function a lot to do my own report creation and analysis. Not everyone will use this functionality, but for Excel nerds, it’s a handy addition.

Reporting Improvements. Reports in Quicken for Mac finally gained the basic and longstanding Windows capability of drilling down to transaction-level detail. The details open in a new window which can be customized and saved as its own report, or exported to Excel. This will be a much-used feature as I prepare my taxes this year. I wish a Budget to Actual report were available in the Mac version, as this drill-down capability would be a big help in more quickly identifying the source of budget variances. Maybe next year.

Other Updates. The Quicken data file is now encrypted on your hard drive, so long as you are using a password to access it. In reading the software release notes, Quicken made some improvements to other areas of the program, but most all of these slipped by me unnoticed. If you use the Bill-Pay feature, things are cleaned up and more intuitive to use. I was flummoxed by the complexity of this service when I first tried it and stopped using it even though it’s a free service as a Premiere subscriber. I feel more confident in paying my bills through my bank’s Bill-Pay feature than Quicken’s offering. This has improved allegedly, though I haven’t tried it again.

What’s Still a Problem

Reporting, Particularly Against Budget. Reporting in the Mac version of Quicken has improved a little, but not near enough. As I mentioned, I still can’t get a report of my income and expense against budget, a staple of the Windows version and basic financial management. Instead, you get a bizarre on-screen visualization of budget performance for the month, or an unwieldy 12 month stacked grid, neither of which I find at all useful. A software engineer without any financial sense must have put these views together. As a workaround, I export actual and budget figures out of Quicken to create a proper actual vs. budget report in Excel. I’ve automated this the best I can, but still takes a time each month to update references and labels, and once in Excel, loses its interactivity and drill-down capability.

Quirky Transaction Download Errors Every time I do an online update of my accounts, I receive the same throttling error for a random set of accounts with my primary bank. I have a half-dozen banking, savings, and credit card accounts with this bank which is apparently too many. I click the “try again,” and the process completes. I’ve researched this error online and discovered that many users suffer from this across a variety of financial institutions. Quicken’s response is consistent: “your bank’s servers must be busy. Try again later.” Downloading transactions in Quicken on Windows was always a tricky proposition, so I can’t say this is a Mac issue. Just irritating. Editor’s Note: These download errors were fixed in Quicken’s August 2019 (version 5.12.3) update. Thank you, Quicken!

Mobile App is Underwhelming. Quicken’s iPad app has been out for a while. I tried it out when it first came out and was underwhelmed. I tried it again for this review, and I am still unimpressed. I’m not alone: the app ratings are abysmal which many reports of the app crashing or not being able to log in. Quicken also released web access in the fall with similar capabilities.

Trapped Investment Data. One of the biggest reservations I have with the Mac version of Quicken relates to its file export limitations. While Quicken promises a “Data Access Guarantee,” the export functionality of the Mac program remains severely crippled. Investment accounts, and all the related historical transaction details, cannot be exported. This limitation affects not only your ability to move back to the more robust Windows version of Quicken should you grow tired of the Mac’s shortcomings, but also impacts your ability to switch to other personal finance software products on the Mac if you decide to give up on Quicken altogether. The lack of this basic export function feels intentional to me to keep customers from leaving the product.

If you are using the Windows version of Quicken and you have investment accounts, you should be very cautious before migrating to the Mac version. You’ll likely be able to move everything over to the Mac, but you’ll be stuck with limited choices of ever leaving. Shame on Quicken for taking our financial data hostage.

Closing Thoughts

So, after all these years, where do I stand with Quicken for Mac?

Like a year ago, I feel like Quicken could be so much better, but it’s still the best software, on the Mac or the PC, for complicated personal finance. Quicken for Mac is good enough that I’m not willing to go through all the work to revert back to the Windows version and deal with running a virtual PC on my Mac. I’m disappointed that my Mac data file can’t export to other software programs. I hope future Quicken versions will finally improve enough to be on par with Windows, though experience makes me very skeptical.

If you’re a Mac user with an extensive investment portfolio, but still on the Windows version, I would recommend staying that more robust software until the Mac version allows proper data exporting.

Are you a Quicken for Mac user, or a Windows user thinking of making the switch to Mac? Let me know your questions and feedback in the comment section below.

Friday, January 5, 2018 • 13 min read

An update to this review for Quicken 2019 for Mac is available here.

Personal financial management is important to me. I’ve always tried to be disciplined when it comes to money, and as a CPA and business planner as my chosen vocation, managing my own money comes pretty naturally. Applying finance strategies I’ve used in managing businesses to my personal finances has paid dividends. Like an accounting system at the office, a well-managed home needs its own financial record keeping. In my case, that system has been the venerable software tool Quicken. What follows is a history of how I’ve used Quicken and reactions to the most recent version of Quicken 2018 for Mac.

Background

I’ve been a user of Quicken personal finance software since 1989. Back then I used a Mac SE, painstakingly capturing every transaction with the proper income or spending category on a nine-inch black and white screen. The discipline of tracking my expenses and using a budget helped me control my spending and keep my focus on long-term financial goals. I’m not exaggerating when I say that I would not be in the financial position I am today without the discipline this software cultivates.

In the 1990s as Microsoft Windows took hold and the days of the Mac waned, I switched over to the PC version of Quicken. My data file had grown so large it no longer fit on a 3 1/2" floppy drive. I couldn’t find an easy way to transfer the data file. Quicken offered a “feature” back then to archive (i.e. erase) your financial history, so in a keystroke, I lost all that meticulous bookkeeping of the previous decade. I’m sad about that now as I would have liked to revisit the financial transactions supporting both by frugality and spending extravagance of my twenties. And remind myself of how little I had back then. Oh well.

I switched back to a Mac at home in 2003. It was fun to return to Apple with a beautiful new iMac at home while I used a Dell laptop for work. Quicken wasn’t available on the Mac at that time, so I kept my financial records on the Dell. This was OK because I had compartmentalized the Mac and PC this way: the Mac was for creative work: movies and photos, writing, games, family time. The PC was all business.

Fast forward another ten years. By 2013 everyone in my family was using a Mac, plus iPhones and iPads. I turned in my work laptop in favor of a MacBook Pro, using a virtual PC software program called Parallels to get access to the short list of PC software titles I still needed: an arcane business intelligence tool for work and … Quicken. A Mac version of Quicken was available, but it lacked many of the features that the PC version, like investment tracking and budgets.

New Mac versions of Quicken would come out every year and I would read reviews by unhappy customers lamenting the awfulness of the software. Buggy, lacked many important features, basically a shell of the PC version. And so I kept using Quicken for Windows along with updates to the VM software and waited.

By last summer, the only PC software I still needed to run on a virtual machine was Quicken. Everything else was native Mac.

Last fall Quicken 2017 for Mac was released. And guess what? The early reviews were positive for a change. I spent about an hour reading up on the new software and decided to try it. I might waste $75, but if there’s a chance it can work for me, I would be able to leave the PC software world for good.

The Transition from Windows to Mac

Installation was uneventful in my case. You can either start from scratch or import an existing Quicken file. I was coming from Quicken 2014 for Windows so I chose that option, found my Quicken data file and clicked proceed. I was worried that this process would somehow corrupt my existing Quicken for Windows data file, so I made to sure to make a complete backup before proceeding with this import, but I needn’t have worried. The process created a new data file for the Mac software while leaving the original unchanged and still usable by its Windows counterpart.

During the import process, I watched the progress bar with some trepidation. Fourteen years of some pretty complicated financial transactions made me think this couldn’t really work. The process took about five minutes during which the familiar account bar on the left-hand portion of the screen progressed from a meaningless gobble of positive and negative balances to finally the exact balances I had in the Windows version. That was a nice way to start.

There were a couple problems. A new mystery credit card account appeared with my name followed by the word TEMP, but it had a zero balance so I didn’t worry about it. Later I found that this was a doubling of an actual credit card account that I had opened and closed in the past five years which resulted in a double-posting of the transactions for that account. Once discovered, it was easy to go back and delete the temporary account transactions, but it took some time to discover and I received no warning messages during the import process that this had happened.

My financial institution account logins and passwords did not carry over from the PC version and it was a little confusing at first to figure that out. Setting up online downloading of transactions was pretty straightforward, and once you get the hang of it, maybe easier than on Windows.

Any budgets I had created in Windows did not carry over to the Mac version. It took about 30 minutes to recreate my budget for this year. The budget creation and edit process are a little clunky but no worse than Windows.

With my accounts fully connected to their respective financial institutions and my budget created, I was able to better evaluate the new user interface and capabilities of the Mac version.

Initial Reactions

My initial impressions were mostly positive. Gone was the incredible bloat of 20 years of features added to the legacy Windows product. I don’t need a built-in credit score checker, college/retirement plan, or a maze of menu options to navigate even the simplest thing.

The Mac version is simpler and has most all the essential features intuitively organized and easy to find. Investment tracking is simple but accurate. The register and data entry tools are far better and fit the retina display capabilities of the Mac whereas the PC version ported through Parallels always needed tweaking just to see your transactions.

Reporting is much more basic and less customizable, but I found I was able to get the information I needed from existing reports and from an onscreen analysis that didn’t exist in Windows. Still, It feels like reporting is a work in progress. There’s also no way that I could find to schedule a loan/mortgage payment based on an amortization table which is a weird omission for a personal finance program (more on this in the next Quicken 2018 for Mac section).

A Year Later: Quicken 2018 for Mac

I continued my trial of using the Mac version of Quicken over the course of the last year, choosing the simplicity of a native application. I learned a lot more about the software’s feature set and a growing list of things I missed from the PC version. I let my Quicken for Windows file languish. After 12 months and a lot of financial transactions later, it would take a tremendous effort to reconstruct my financial world in that PC software, so I resigned myself to deal with the good and the bad of the Mac version of the software.

In November, Quicken released a new version for the Mac, Quicken 2018. I waited four weeks to purchase a subscription (more on this later) after reading many, many negative reviews of the update, mostly about the outrage customers felt about being forced to pay each year for a substandard piece of software.

Quicken’s decision to move to a subscription service, alongside so many other software developers this year, didn’t surprise me. In fact, I already considered Quicken a subscription service after having to upgrade every two to three years just to keep bank and credit card downloads working properly. I bought a 27-month subscription from Amazon.com during a Black Friday sale which worked out to be roughly $35 per year for the Premium edition of Quicken. I now have a license for both Mac and PC if I choose to somehow migrate back. That’s like buying the software every two years which is about what I have done over the past decade. I’m OK with this, though I know many, many other customers are upset. In my view, the developers of Quicken have an opportunity to use this steady income from subscriptions to finally make the necessary improvements to the Mac version after so many years. However, if they fail to make improvements and continue to hobble the product after now forcing customers to pay annually, this will hasten their demise, at least on the Mac platform. Quicken developers: you better get to work!

The Premier subscription of Quicken includes free BillPay services and premium telephone support. I made use of this support service after discovering that Quicken was charging me $9.95 per month for BillPay while it should have been free. My phone call was answered promptly and helpfully, and while they couldn’t solve me BillPay issue (I had to call another number and waited 45 minutes on hold), I was pleased to know I can pick up the phone and quickly speak to a technician when I next encounter a Quicken problem.

Once Quicken 2018 for Mac was installed, I had a hard time finding many changes. Loan amortizations are now supported, along with some small changes to investment tracking and bill paying. No improvements to reporting though which I consider to be the biggest drawback of using the Mac.

Take, for example, the common actual vs. budget report that I’ve used to manage my finances for decades. It’s a pretty simple layout: actual, budget and a variance for the current month and year to date. For business or for personal finance, this is the most basic way of measuring whether you’re on plan or not. In Quicken for Windows, this is one of the default reports. Not so in the Mac version. In lieu of a budget report, you get either a grid view of your monthly budget interlaced with actual results, useful if you want to update your budget or a graphical display of one particular month vs. budget which takes up a whole lot of space without conveying much information. Not very useful. As a workaround, I export actual and budget figures out of Quicken to create a proper actual vs. budget report in Excel. I’ve automated this the best I can, but still takes a time each month to update references and labels, and once in Excel, loses its interactivity and drill-down capability.

Another example of reporting shortfalls came to light when I prepared my taxes earlier this year. Quicken tracks all my expenses by category and I needed a simple report of all my charitable contributions for the previous year broken down by payee. Simple, right? In Quicken for Windows, it would have been automatically provided for me by simply drilling down from my summary budget report for the year. In the Mac version, it’s not so easy. After a lot of tweaking, I was able to create a summary report summarized by payee for a particular category, but the report, understood only by a non-finance developer, did not include a total. So, if you flipped through my tax return support for last year, you’d see totals added in pencil for every supporting schedule on my tax return. So basic, and yet still unresolved on the Mac these many years.

Or, how about suppressing zero balance rows in reports? So basic, yet missing. Reporting in Quicken for Mac remains a big disappointment to me in using the software.

Another pet peeve is Quicken’s amnesia when it comes to auto-assigning categories to downloaded banking transactions. I pay the same utility company every month, yet inexplicably, Quicken fails to categorize the transaction. I have to go in and update the transaction with the proper category. This happens with a half-dozen routine expenses, yet many other transactions, particularly from credit cards, are categorized correctly. Perhaps all the bloat of 14 years of financial history in my situation has complicated things, but still … this is such a basic feature in Quicken for Windows that I scratch my head in wonder with the Mac version.

Quicken for Mac has an auto-backup feature, similar to Windows, but is much more intrusive to the user. Every time you quit the program, it launches a dialog box with a spinning gear while it backs up, taking over your system while it works, visible even if you move to another application. In Windows, this was completely invisible. Sloppy programming on the Mac.

Performance is OK, even with a fairly large data file of financial history, but any transaction searches will result in a beach ball delay for a few seconds. Just slightly annoying vs. the zero delay in the Windows counter-part. I’m running Quicken on a new souped-up iMac, so others with older computer hardware might find that performance suffers much more on the Mac.

Welcome to the Hotel California

Perhaps the biggest reservation I have with the Mac version of Quicken relates its file export limitations. As I described earlier, the process of exporting a Quicken to Windows file to the Mac worked pretty well. However, the reverse process of going from the Mac to Windows, considered now an industry file standard for personal finance software, has serious limitations. Investment accounts, for example, simply won’t transfer. In my test to go from Quicken 2018 for Mac to Quicken 2018 for Windows, I had an astounding 26,000 errors which resulted in a Quicken data file that was completely unusable. This limitation affects not only your ability to move back to the more robust Windows version of Quicken should you grow tired of the Mac’s limitations, but also impacts your ability to switch to other personal finance software products on the Mac if you decide to give up on Quicken altogether. The lack of this common export function feels intentional to me to keep customers from leaving the product.

If you are using the Windows version of Quicken and you have investment accounts, you should be very cautious before migrating to the Mac version. You’ll likely be able to move everything over to the Mac, but you’ll be stuck with limited choices of ever leaving. This is probably the biggest disappointment I have with Quicken 2018. Shame on Quicken for taking your financial data hostage.

Closing Thoughts

So, after all these years, where do I stand with Quicken for Mac? I’d summarize my current feeling as grudging acceptance. Quicken for Mac is good enough that I’m not willing to go through all the work to revert back to the Windows version and deal with running a virtual PC on my Mac. I’m disappointed that my Mac data file can’t export to other software programs. I hope with a subscription revenue stream that future Quicken versions will finally improve enough to be on par with Windows, though past experience makes me very skeptical. If you find yourself a guest in this Hotel California, stop by and say hello.

{kind=link}